Platinum Wealth

-

Posts

623 -

Joined

-

Last visited

-

Days Won

24

Content Type

Profiles

Forums

Events

Articles

Everything posted by Platinum Wealth

-

What is the link to the image you tried to post? It was base64 encoded so basically the url was so long it broke the layout pushing the edit button off canvas.

-

It sure is: And it is still so small compared to the bigger picture of $338,462,809,191 Crypto Market Cap Source: CoinData SA

-

Sounds like a pyramid.

Sounds like a pyramid. -

Every year, Just One Lap founder Simon Brown uses the last Power Hour to look at what we can expect from the year ahead. First, he’ll review how accurate the previous year’s predictions have been before turning his attention to 2018. 2017 has been a turbulent year for global politics, but markets have been strong. Many markets have hit repeated all-time highs. Even local markets were having a good year, despite many distractions on the economic and political front. Looking ahead to 2018, Simon will focus on local and global economic and political events. He’ll discuss how he expects these to affect markets, commodities, currencies and interest rates. He’ll also look for some local shares that might be worth considering within the context. End your financial year on a high note with the JSE, Just One Lap and our Power Hour speakers. Stick around after the presentation to celebrate the end of 2017 with a drink. Register for the free webinar here -> https://register.gotowebinar.com/register/7030875868408580355

-

Guess this is as good a place as any, I removed the ICO and Other Cryptocurrency section from showing up on the latest threads sidebar, the thinking was that this is a finance (albeit traditional) forum first and most of the users landing on the forum are simply not that interested in foreign concepts, it's still available and will remain here, but the front page will be tailored for traditional finance.

-

Somehow it feels too little too late - https://www.iol.co.za/business-report/watch-durbanites-flock-to-the-new-starbucks-12050569

-

Cape Town - Magda Wierzycka, the CEO of fintech company Sygnia Asset Management, has secured a High Court ruling ordering ANN7 owner Mzwanele Manyi to remove a number of Twitter and Facebook posts. The judgment was handed down in the Gauteng Local Division of the High Court in Johannesburg on Monday by acting High Court Judge Fiona Dippenaar. However, Dippenaar also referred the matter to a single judge sitting as an Equality Court and a High Court to make a final ruling. In her order Dippenaar wrote that pending a final ruling on the matter, Manyi must remove, within 24 hours, statements that Wierzycka said were defamatory from his social media accounts. Manyi has also been barred from making, retweeting or commenting on “defamatory statements” concerning Wierzycka or Sygnia. In a WhatsApp on Monday evening, Manyi told Fin24 that he was waiting for his attorney to send him the judgment. ‘Economic terrorism’ Wierzycka had filed an urgent application in the South Gauteng High Court in early September after Manyi wrote on Twitter and Facebook that she was guilty of "economic terrorism" and was a “downright racist”. This followed an interview that Wierzycka did on CNBC Africa in early April 2017, where, among other matters, she said she would offer President Zuma as “much money as he wishes to have” to step down to boost investor confidence. Manyi, on social media, then claimed that Wierzycka wanted to “buy off” the President, tweeting that she “objectifies black people as things that can be bought”. He also referred to her as a “super-rich White Monopoly Capitalist” and in a separate tweet said he wondered whether she was related to Janusz Walus, the man who assassinated SACP secretary general Chris Hani in 1993. In her judgment, Dippenaar said Manyi defended himself, in part, on the basis of freedom of expression. “He contends that the applicants are attempting to suppress fair comment on socio-economic issues which do not accord with the first applicant’s [Wierzycka] own views”. Lawyers for Wierzycka, meanwhile, said as part of their broader arguments that, as a public figure with many social media followers, Manyi had a special responsibility to ensure his public statements are “well-considered” and do not cause harm or incite violence. 'Balancing exercise' In her 34-page judgment, Dippenaar noted that the case concerned a “delicate balancing exercise” between the right to freedom of expression on the one hand and the right to dignity and equality on the other hand. Dippenaar also said that it was clear that “this court does not have the necessary jurisdiction to determine the application as a whole or consider the granting of any final relief", therefore, refore referred the matter to a single judge sitting as both an Equality Court and as a High Court for final ruling. Source: Fin24

-

When a home seller or, more commonly, their conveyancing attorney applies for a rates clearance certificate from the local council so as to be able to transfer the property to the new owner, the council is by law entitled to recover arrears only going back two years. Any unpaid rates incurred in earlier periods remain a “charge upon the land”, which in South Africa has until now been taken to mean that the new owner becomes liable for them, says Rowan Alexander, Director of Alexander Swart Property. This is, however, seldom made clear to the new owner: mention is not made of historic overdue arrears in the rates clearance schedule. The new owner, therefore, often finds themselves confronted with a possibly large debt which they had not foreseen. Quoting Robert Krautkamer of Miltons Matsemela Attorneys on this matter, Alexander says that to bring about payment of the additional arrears, the council was previously allowed in SA law to disconnect the services to the new owner or to take legal action against them. Councils could even go so far as to auction the property. In such cases, Alexander says the new owner usually somehow found the means to pay the outstanding amount, but was then faced with the often daunting task of trying to reclaim from the seller the sums paid out. A few months ago, however, Alexander says a case of this kind ended up in the Gauteng High Court. They ruled that such actions on the part of the council are unconstitutional, and they referred the matter to the Constitutional Court for a final decision. This Court has now confirmed that such action is, in fact, unconstitutional, and must cease henceforth. Alexander says this means councils will no longer be able to recover arrears older than two years as a “charge upon the land”. They will have to get the sums owed from the previous owner who in fact in most cases incurred the debt, and until this is achieved the new owner will not be allowed to use the property as a security for any other debt. Alexander comments that this is a victory for all property owners: they can now feel more secure about their own position. He says this is also a victory for the banks as they will no longer find their mortgage bondholders suddenly facing possibly large unforeseen expenses. Municipalities unable to produce accurate figures at the time of transfer will probably have to write off the major portion of these outstanding debts, says Alexander. Source: Property24

-

As the holiday season approaches, most of us are counting the days until that yearend bonus hits our account. There’s nothing quite like a little bank balance booster to get us in the holiday spirit. Of course, splurging all that extra cash on impulse buys is probably not the smartest move with costs rising. Wouldn’t it be great if there was a way to make our yearend bonuses work as hard for us as we did for them? Tony Clarke, Managing Director of the Rawson Property Group, says this actually easier than you might think. Here is his 3-step guide to making your bonus go further than ever before, without having to give up all your holiday spoils: 1. Invest a portion “For anyone with a home loan, the smartest thing to do with any extra income is always going to be to put it into your bond,” says Clarke. “It may not be as much fun as splurging on some immediate luxuries, but if you look at it in the long term, it really is the best way to get the most out of your money.” By putting a single lump sum of just R1 000 extra into a R1 million bond, Clarke says homeowners can save as much as R6 000 over the course of their loan. “That R1 000 literally works six times harder for you if you put it into your home loan,” he says, “and the more money you invest that way, the bigger the savings.” 2. Save a portion Bond repayments aren’t the only cost homeowners have to shoulder - maintenance and upgrades are also essential if you want to retain the value of your home as an investment. Because of this, Clarke suggests setting aside a portion of your year-end bonus for home improvements. This, he says, is a great way to get tangible benefits from your money while also increasing the value of your property. “I generally advise homeowners to budget between 5% and 10% of the value of their property every year to keep things ship-shape, up-to-date and easily resalable,” says Clarke. “By putting some of your bonus towards those expenses, you can not only enjoy the improvements you make, but also increase your potential profits if and when you decide to sell.” Some improvements are more likely to see good returns than others, so Clarke recommends chatting to a real estate professional in your area before going ahead with renovations. “You have to keep buyer preferencesprioritizingn prioritising improvements,” he says. “Things like rainwater harvesting and greywater systems are becoming very sought after in the Western Cape, while built-in braais and outdoor entertainment areas are popular all over the country. If you can tap into these trends with your renovations, you could see exponential returns on your investment.” 3. Splurge a portion It wouldn’t be a bonus if we didn’t splurge at least a little of it on non-essentials. For those of us with an interest in home décor, however, clever splurges can do double duty. “If you’ve been dreaming of new bed linens, better curtains, or that family photo wall, your bonus could be just the cash injection you need to finally spoil yourself,” says Clarke. “These kinds of décor items make cherished gifts that can last for years to come, keep your space looking fresh and modern, and help turn any house into a home.” Source: Property24

-

Zanu-PF has formally notified under-fire Zimbabwean President Robert Mugabe on Monday of the decision to recall him from the ruling party. “Pursuant to the decisions of the Zanu PF central committee entered on November 19, 2017 recalling Cde President Robert Gabriel Mugabe from the position president and first secretary of Zanu PF, the party wishes to announce that Cde R G Mugabe has been formally notified of the decisions this morning,” Zanu-PF secretary for information Simon Khaya Moyo, said in a statement. “As for that, the party has instructed the chief whip to proceed with impeachment process against Cde R G Mugabe as it has not received the anticipated confirmation of his resignation from the Speaker of Parliament. A caucus of Zanu PF parliamentarians is currently underway in pursuit of the resolutions by the special session of the central committee to initiate impeachment processes. “The motion of proceedings is expected to be tabled before Parliament when it seats on Tuesday, November 21, 2017.” Legal think-tank Veritas said that once the Senate and the National Assembly, sitting jointly, have passed a resolution that the president should be removed from office, he immediately ceases to hold office in terms of Section 97(3) of the Constitution. “In trying to work out a likely scenario, we must remember that at its meeting yesterday the Zanu PF central committee declared Mr [Emmerson] Mnangagwa to be the party’s candidate for President. So the party does not have to wait for its congress in December to make a nomination. It has already done so," it said. “If, therefore, Parliament does resolve in terms of section 97 of the Constitution that Mugabe should be removed from office, the consequences will be: Mugabe immediately ceases to hold office as president; [Phelekezela] Mphoko, the sole Vice-President, will take over as acting president.” Veritas said the fact that Mphoko may be in detention or outside the country does not matter: his assumption of office will be automatic, and will not depend on his taking an oath of office. “If Mphoko is persuaded to resign or is impeached, this will not happen, because he will cease to be Vice-President upon his resignation or the passing of the impeachment motion. Even if Mphoko does not resign or is not impeached, his term of office as Acting President may be fleeting, and will depend on how soon Zanu PF can notify the Speaker that it has nominated Mnangagwa as Mugabe’s successor,” the legal think-tank said. Veritas said that this might be no longer than the time it would take for Zanu PFs chief whip to hand in the nomination notice to the speaker and once that is done Mnangagwa will become president and will assume office when he is sworn in by the Chief Justice. “The new President will hold office until the next general election, which should be held not later than August 23, 2018," it said. “Upon the assumption of office by the new President ‑ ie when he is sworn in ‑ all current ministers and deputy ministers will go out of office in terms of section 108(1)© of the Constitution. They will, however, be eligible for re-appointment when the new President appoints his own ministers.” Source: IOL

-

Hello Mr Tourist, welcome to the forum!

-

Forum Updates and Forum Status

Platinum Wealth replied to Platinum Wealth's topic in Site News & Feedback

We changed the default color scheme of the website. We change the layout of the login box Old New We change the overall color to the following and added a banner visible to guests.

-

South Africa’s rand tumbled more than 1% and the risk premium on government bonds soared on Monday over news of a top Treasury official resignation, financial woes at the sole power utility and political jostling in the ruling party. A report by a presidential commission that government raise spending on higher education saw muted response from markets, with traders saying it was short on detail. The rand, which weakened after the presidency said it would release the commission’s findings at midday, was little changed after it was published. It slipped to a one-year low on Friday amid reports President Jacob Zuma was preparing to introduce free higher education, which would put added pressure on public finances. At 1120 GMT the rand was at 14.5200 per dollar having tumbled as much as 1.1% to session-worst 14.5425, its weakest level since Nov. 18 2016. Government bond due 2026 also weakened. Yields on the paper climbed 14.5 basis points to 9.495%, its highest level since May 2016. South African 5-year credit default swaps, a measure of the cost of insuring the country’s debt, hit a four-month high, stoked by reports of power firm Eskom’s financial troubles. Eskom said it was not insolvent but was facing serious liquidity issues. Treasury confirmed Michael Sachs’ resignation, saying he wanted to join the civil service in a different capacity. Fin24 said Sachs resigned over interference by Zuma at the Treasury. “The rumour that a senior treasury official has resigned is obviously the main reason the rand moved lower,” said chief dealer at Bidvest Bank Kumeran Govender. “But they’re also reports that ANC Secretary-General Gwede Mantashe is under pressure and that hasn’t helped either.” Local news reported that Mantashe was facing calls to quit by some members of the party. The ANC denied the claims. On bonds, Govender added that fund managers, particularly from primary dealers, were offloading debt ahead of a government bond auction on Tuesday where Treasury will increase issuance. Senior currency dealer at Standard Bank Oliver Alwar said investors were jittery over the rumours of Sachs resignation and increased government spending on higher education ahead of visits to South Africa next week by ratings agencies. “It’s looking more and more likely that we will be downgraded,” Alwar said. Stocks firmed, with the Top 40 index up 0.52% to to 53,706 points, and the wider All-Share index 0.42% firmer at 60,027 points. Source: IOL

-

Cape Town - After much anticipation, President Jacob Zuma on Monday released the findings of the Heher commission, which investigated the possibility of providing free higher education in South Africa. Here are 10 things you need to know about the fees commission report. 1. The Commission recommended that government increase its expenditure on higher education and training to a minimum of 1% of the GDP. 2. It wants government to adopt a cost-effective plan to develop more student accommodation and historically-disadvantaged institutions should be a top priority. 3. Government has been asked to investigate the viability of "online and blended learning" as an alternative to formal study, due to capacity issues at many institutions. 4. With regards to TVET colleges, the commission recommended that students should receive fully subsidised free education in the form of grants. 5. The Commission recommended that post-graduate students have access to a cost-sharing model of government guaranteed Income-Contingency Loans sourced from commercial banks (ICL). 6. Students with debt, but who have already graduated, should be offered income-contingent loans (ICL) as well. 7. The Commission recommended that the current National Student Financial Aid Scheme (NSFAS) system be replaced by the ICL system. 8. According to the Commission, undergraduate and postgraduate students studying at public and private universities and colleges, should be funded through the ICL system. 9. The Commission called on the scrapping of application and registration fees. 10. The Commission recommends that commercial banks issue government guaranteed loans to students that are payable upon graduation and repayment only starts when the student reaches a certain threshold income. Source: IOL

-

Pretoria – A hibiscus tea set from Omar Al Bashir, Parker pens from Richard Mdluli, wine from Vladimir Putin and Nguni cattle from Mugabe, but no declaration by President Jacob Zuma of a R1 million a month salary by Roy Moodley, as alleged. DA leader Mmusi Maimane on Monday viewed Zuma's declaration of interests at the Union Buildings in Pretoria. In the President's Keepers - a book by Jacques Pauw, the author details how a SARS official in 2010 discovered that Zuma had been receiving payments of R1m a month from Royal Security, a company owned by Durban businessman and ANC-supporter Roy Moodley. Moodley allegedly bankrolled Zuma for at least four months after he became president in 2009. According to Maimane, the only declaration made in respect to Moodley is when the businessman allowed Zuma to use a property on the Durban beachfront in 2016. "I can today confirm that President Jacob Zuma did not declare any salary earned in the 2009-10 financial year in the register of his financial interests," Maimane told reporters. Maimane added that there were no declarations made in relation to Zuma's former financial advisor Shabir Shaik, "which became part of the record when it came to the president's report in the court case against Shaik". "The president also made no declarations of the loan that he would have got in the upgrades in the Nkandla matter." Maimane was referring to the VBS Mutual Bank that granted Zuma a R7.8m loan to repay some of the security upgrades at his homestead in KwaZulu-Natal. More gifts Furthermore, Maimane said there were no declarations made of directorships or shareholdings by Zuma or any of his wives. There were also no declarations made in relation to the controversial Gupta family, however, Zuma did declare that he has received a number of Nguni cattle and art from Zimbabwean President Robert Mugabe. Zuma also received a "silver watch" from Black Management Forum by Jimmy Manyi and a gold watch by the United Arab Emirates, both watches did not have their value declared - another bone of contention, said Maimane. He received two Parker pens from suspended Crime Intelligence Head, Richard Mdluli, four bottles of wine from Russian President Vladimir Putin in 2016 and a tea set from Sudanese President Omar Al Bashir in 2014, a year before Al Bashir was allowed to enter and leave the country despite being wanted for crimes against humanity. "What was obvious of concern is why the president is receiving gifts from a person who is wanted for crimes of genocide and killing of African people, it's clear that the president was willing to get gifts from anybody," said Maimane. Maimane said he would be submitting applications in terms of the Promotion of Access to Information Act (2 of 2000) to gain access to Moodley's employment records and to gain access to private declarations that Zuma may have made. He will also be laying a complaint with the Public Protector. "Somebody is lying and I am not willing to say that Mr Pauw is lying, it must be investigated thoroughly." Source: News24

-

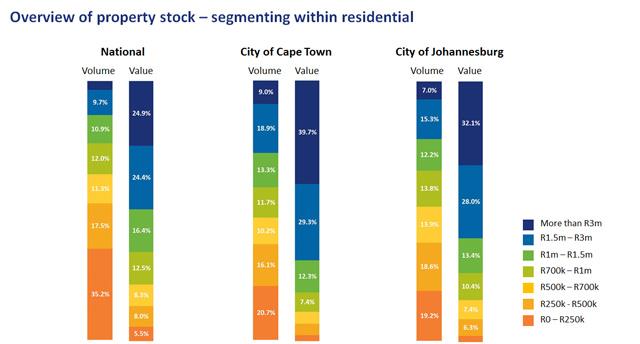

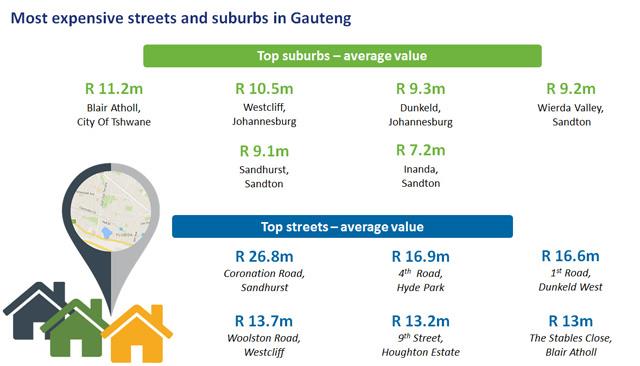

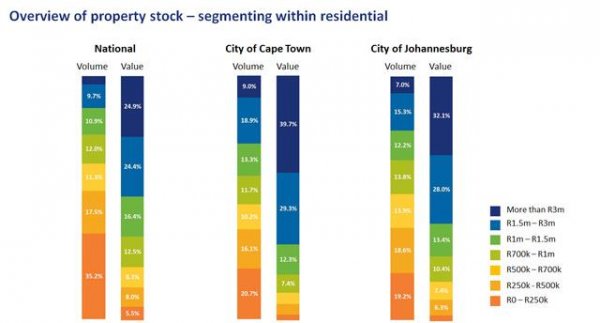

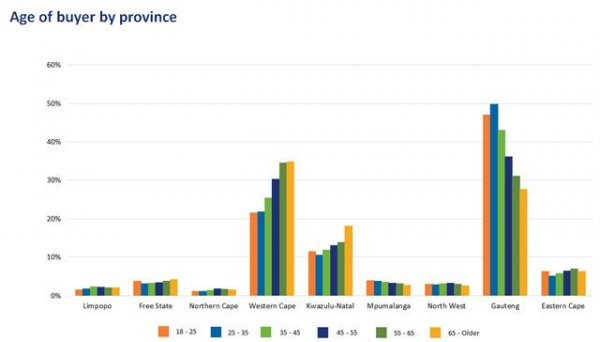

Property remains one of the oldest and most popular investments globally, and property forecasters have recently mentioned that the biggest deterrents for buyers are not only the economy, but having confidence in the location of the property. Lightstone provides analysis to evaluate trends and segmentation within the property sector, which includes the data of 7.9 million registered properties across South Africa, 6.5 million of which are residential properties valued at R5 trillion. Freehold properties make up the biggest portion at 69.7%, then estates (15. 5%) followed by sectional title (14.8%). Estates consist of a much higher proportion of total value vs. volume as these properties are on average, valued at three times more than normal freehold properties. It’s no surprise given that even though Gauteng is the smallest province, it is home to the biggest portion of total properties in both value and volume, while the Western Cape comes in at number two and KwaZulu-Natal at number three, according to Lighstone. Gauteng and the Western Cape include more than half of all properties (6.5 million) and two thirds of the total value (R5 trillion). As the biggest province, the Northern Cape is still the least developed residential province with less than 1.3% of the total value of residential properties. Residential property stock segmentation Like Cape Town, Johannesburg has a much larger proportion of properties in the upper value band with almost one third of properties worth over R3 million. The increased property growth in Cape Town can be attributed to the migration of Gauteng residents and the landlocked nature of the city, says Lightstone. Sectors like the interior Atlantic Seaboard and Southern Suburbs have sustained growth of very high valued properties. Lightstone data also sheds light on the most expensive streets and suburbs in Gauteng, and surprisingly the number one spot belongs to Blair Atholl, situated in the City of Tshwane. Coronation Street in Sandhurst is highlighted as the most expensive street at an average value of R26 million per house. Analysis of estates in Gauteng shows the highest median value at Clouds End in Sandton and the highest inflation at Willow Grove in Witkoppen. When comparing the average age of buyers in the top ten suburbs offering the highest number of first-time buyers, it is encouraging to see that Soshanguve South and Protea Glen have the most growth. The age of buyers in Gauteng is between 18 and 55 years old, which shows us that the younger working class is investing in property. “Cape Town shows its biggest growth in property buyers over the age of 55 to 65, as well as 65 and older indicating that an older generation is looking to establish themselves in this province for what we can assume to be for retirement,” says Lightstone. Source: Property24

-

Cape Town is following the trend seen in cities such as Berlin, London, New York, Barcelona and Paris, and is set to see the development of the first state-of-the-art micro-living apartments in the city. To be constructed at 1 Albert Road in Woodstock, these micro units will range in size from 21sqm studios to 75sqm two bedroom units. All the apartments will feature top-end SMEG appliances, flat screen smart TVs and uncapped, unshaped 100megs per second fibre internet, to name but a few of the features. Rob Stefanutto, Managing Director of Dogon Group Properties, explains that in addition to the 133 living units over seven floors, the 1 On Albert development will also feature communal recreational spaces, shops, a food court, laundromat, heated swimming pool and more. “All part of a new conceptual design in living known as integrated living solutions, which incorporates all the elements needed for inner-city living without having to leave the building.” The 1 On Albert building, which is centrally situated in the up-and-coming area of Woodstock on a MyCiti bus route and with an Uber point at its doorstep, has been designed by award-winning architects Louis Karol, and the interiors of the apartments designed by leading hotel room designer Grant Gillis of Delta Interiors. First-time buyers able to enter the property market “Micro living units have been popular internationally for several years, and we are now following this trend in Cape Town. Millennials are looking for location over square footage - they want to be close to the city centre, close enough to walk, bike, or rely on public transportation,” says Stefanutto. “However, with cities becoming increasingly overcrowded there is not only a shortage of housing, but also the cost of properties has skyrocketed to such a point that young people cannot afford to buy their first property and get onto the property ladder - forcing them to rent on an ongoing basis.” Recognising this, he says 1 On Albert, which is the first offering in a collaborative partnership between Dogon, AJ Developers, Power Construction and Gardner Property Solutions, has been designed to let the consumer buy their first home, with Nedbank having come on board to offer flexible finance that includes reduced interest rates, discounted registration fees and flexible deposit options. “The key to the value chain in real estate is to get on the property ladder as early as possible, and 1 On Albert is providing the missing link to the property value chain,” says Stefanutto. The entry-level units at 1 On Albert are priced from R799 000 (sold out) to R945 000 inclusive of transfer duty. This equates to a monthly bond instalment that is in line with, if not lower than, rental figures. Those earning between R18 000 and R25 000 per month should qualify for finance through Nedbank. “At these asking prices, when buyers eventually sell to move up the property ladder, they will in all likelihood not face any Capital Gains Tax if they have been living in the unit as their primary residence. This, coupled with no transfer duty and reduced bond registration costs, means that there is minimal investment leakage for buyers - further helping them to climb the property ladder,” says Stefanutto. Stefanutto further explains that another benefit of these micro-living units are the low monthly levies and rates, a cost which, in the case of many other developments, creates a barrier for budget-conscious first-time buyers. A significant development for Cape Town’s property industry “It is necessary for the property development industry to produce an ever-changing and adapted product that fulfils the needs of consumers, and I feel that 1 On Albert is one of the most significant developments to hit the property market in the 20 years that I have been in the industry,” says Stefanutto. “Dogon Group are very excited to be a part of this project which allows us to introduce a whole new segment of customers to the property market through entry-level units which are still in keeping with the upmarket, top-end style of properties which Dogon is synonymous with.” Construction on 1 On Albert will begin in February 2018, and units have already started to sell “in this exciting development which is seen as the gateway project for the emerging suburb of Woodstock - a suburb which has seen ongoing revival in recent years and offers direct access to the city centre,” says Stefanutto.

toR945000inclusiveoftransferduty.thumb.jpg.28b66c29a4a656d71eb56db1db64e87d.jpg)

-

Personally, I won't climb in now.

-

Many first-time buy-to-let investors spend a good deal of time considering whether a rental agent is the best option for managing their property, or if they could successfully handle the letting of their investment on their own. While there are pros and cons to both options, Jacqui Savage, National Business Development Manager for Rawson Rentals, says the benefits of using an experienced and trustworthy rental agent will, for the majority of landlords, far outweigh the self-managed alternative. “Managing a property yourself is not only extremely time-consuming,” Savage explains, “but requires a great deal of knowledge of some quite complex laws and regulations put in place by the Rental Housing Tribunal. South African law tends to err on the side of protecting the tenant, not the landlord, and if your contracts and communications with the tenant don’t fall 100% within the rules from day one, you can quickly find yourself on the wrong end of an expensive dispute.” “As a private individual, it can be much more difficult not only drafting a solid lease agreement to protect everyone involved, but performing the necessary background checks to distinguish between good tenants and bad,” she says. “Credit checks, for example, are absolutely vital, but can be difficult to action as a landlord in your personal capacity. High-risk tenants are often aware of this fact, and are not above taking advantage of it when they can.” By using a reputable rental agent, Savage explains that you have access not only to their tried and tested lease agreements, but also their stringent background checks, processes, and hard-earned experience that dramatically reduces the likelihood of signing a delinquent tenant. In the event that you do end up with a less-than-stellar lessee, however, your agent will also be able to help minimise the impact by streamlining the collection and, in extreme cases, eviction processes. “Trust and reliability is the biggest concern we see from landlords who are considering using a rental agent to manage their property,” Savage admits. “Handing over responsibility for one of your largest assets is understandably daunting, and you can imagine why landlords might be nervous about trusting a stranger with something that important.” “Fortunately, there are ways to mitigate your risk when contracting a rental agent. Word of mouth referrals are invaluable – a successful track record speaks volumes of a rental agent’s experience and dedication – but the most important thing to do is to check their credentials.” All rental agents are legally required to have an annually updated Fidelity Fund Certificate (FFC) in order to trade, and must be registered with the Estate Agency Affairs Board (EAAB). “If your rental agent can’t provide proof of both, walk away and find one who can,” says Savage. Costs are the other main issue raised by landlords considering the services of a rental agent, and many questions whether the time and effort saved are worth the extra expense. “What landlords might not realize,” Savage explains, “is that part of the rental agent’s responsibility is to run your property in the most efficient and profitable way for you. With the right tenant management, maintenance, and rental escalations, your property will generate more income under a good rental agent than it would under your own care. “Add to this the decreased likelihood of non-payment and subsequent litigation costs, and that small monthly agent fee suddenly seems like a very good deal.” All signs certainly point towards using a rental agent for your investment property but, should you have any doubts, Savage recommends talking through your options with a few shortlisted candidates. “Ask all the questions you need to, and take your time making a decision. The right agent makes all the difference, so make sure they tick all the boxes you need to feel completely comfortable and confident in their skills and dedication.” Source: Property24

-

With the rising prevalence of buy-to-let investors purchasing sectional title units to build a rental portfolio and the increasing numbers of them also renting out units as short-term accommodation, often to holidaymakers, there is a need to remind owners that they must make their tenants aware of the conduct rules of their scheme. This is according to Mandi le Roux, operations manager of sectional title finance company Propell, who says whether it is an owner-occupant or tenant, the same conduct rules apply, and these should be handed to any new occupant before they move in so that they know they are bound by these rules for the duration of their stay. In this way, she says they cannot plead ignorance if they are reprimanded or fined by the body corporate for misconduct or breaching the rules. Various provisions within the Sectional Titles Schemes Management Act, Prescribed Management Rules (PMR), and Prescribed Conduct Rules (PCR) refer to and bind owners and occupants. While “occupier” is not a defined term, it would include short-term tenants. PMR 3(2) states that a member (owner) must take all reasonable steps to ensure compliance with the conduct rules by any tenant or other occupant of any section or exclusive use area, including the member’s employees, tenants, guests, visitors and family members. This is supported by section 10(4) of the STSMA, which provides that a scheme’s rules “bind the body corporate and the owners of the sections and any person occupying a section”. PCR 7(4) states that: “The owner or occupier of a section is obliged to comply with these conduct rules, notwithstanding any provision to the contrary contained in any lease or any other grant of rights of occupancy”. A landlord, while not directly responsible for his tenant’s behaviour, as the owner of the unit where the occupants resides, will still receive any fines issued from the body corporate for misconduct or breach of rules, and will then have to recoup these from tenants in some way. Everyone needs to adhere to the conduct rules of their scheme so that other residents are not inconvenienced or disturbed, says Le Roux. Source: Property24

-

ABUJA (Reuters) - Nigeria's Senate approved on Wednesday a report largely exonerating South African telecoms company MTN Group Ltd's Nigerian unit, after the business was accused of illegally repatriating $14 billion to its parent. But the Senate report also asked Nigeria's central bank to sanction Stanbic IBTC Bank "for improper documentations in respect of capital repatriation and loan repayments" on behalf of MTN. Parliament's upper house agreed in September last year to investigate whether Africa's biggest telecoms firm unlawfully repatriated $13.92 billion from Nigeria - its most lucrative market which generates a third of its revenue - between 2006 and 2016. A spokesman for MTN said: "We welcome the report. We will study it in more detail. As we've placed on record previously, we have always insisted that our actions have been compliant with the law in this regard." Stanbic IBTC did not immediately respond to an email requesting comment. The senate investigation did not receive proof of collusion to contravene Nigeria's foreign exchange laws, according to the report. "There was evidence of massive capital outflow but that fact alone is not conclusive that a crime has been committed," the report said. As for the Central Bank of Nigeria, the senate committee said its failure to properly regulate foreign exchange should be condemned. The bank should propose amendments to current regulation to foster economic growth and improve Nigeria's foreign currency inflows, said the report. In July the Senate had rejected an earlier version of the report, asking for further work to be undertaken.

-

By Paul O’Sullivan Please read this extract from Jacques Pauw’s book. He’s talking about what he calls, the ‘keepers’. I’m not afraid of any man, and do not require to be anonymous. I gladly admit that I gave Jacques lots of information and led him to others that could get more. I am proud to have played my part and invite anyone who thinks they can stop me from exposing the criminals in the criminal justice system to come and do so. Not Vlok, Mlotshwa, Mabula, Kgorane, Ncube, Mashuga or any of the scum out there can survive what is coming. Good will triumph over evil. It always does. Instead of skulking in the shadows and pretending you do not know what is going on, the rest of you should make a decision and decide now, go down with the sinking ship and end up in prison, or stand up and do what you are constitutionally obligated to do. Michael Hulley, Duduzane Zuma, the Guptas, Yusuf Kajee, the Bhanas, Phahlane, Ntlemeza, Mdluli, Nhleko, Krejcir, not one of these people can or will help you. Their time is nearly over and they will go to prison. You just have to decide if you will join them there, or do what you are supposed to do and honour your country by doing the right thing. I invite all of you to ask yourself how you will be remembered, either as ‘part of the problem’, or ‘part of the solution’. As you start thinking about the cold reality of time in prison, think how you might see the light and become the change that is needed to save this country from evil. Not only will you save yourself from prison, and your family from poverty and shame, you might even help save the country.

-

Dear Residents, Best Regards, Cllr. Ernst Botha Media Alert 06 November 2017 STREETS AFFECTED BY A NATIONAL TAXI ALLIANCES MARCH ON WEDNESDAY 08 NOVEMBER 2017 The Tshwane Metro Police Department would like to notify the Tshwane Citizens about a march that will take place on Wednesday 08 November 2017 by the National Taxi Alliances. The marchers will gather from 09:00 at Old Putco Depot in Marabastad and move from 11:30 to The Department of Transport at Corner Struben and Bosman Street to hand over the first memorandum at 12:00. From the Department of Transport, they will proceed to the Union Buildings where they will hand over the second memorandum at 13:00. The route of the march is as follows: From Old Putco Depot they will turn into Struben Street then proceed straight until they reach the Department of Transport at Corner Struben Street and Bosman Street. They will then use the following route to proceed to the Union Buildings: From Struben Street they will proceed straight then turn right into Nelson Mandela Street and then turn left into Madiba Street until they reach the Union Buildings. They are expected to move back to Old Putco Depot at 14:30 using the following streets: • Madiba Street • Nelson Mandela Drive • Johannes Ramokgoase Street Metro Police officers will deployed to monitor the march and all affected streets. Motorists are advised to avoid the affected streets and use alternative routes such as: • Nana Sita • Francis Baard • Boom Street Issued by the Tshwane Metropolitan Police Department communication Unit

-

Britney isn't metaaaaal

-

Should we make a thread about music? Like The rock thread, metaaaaaaaal etc?